[ad_1]

LendingClub launched its earnings for the primary quarter of 2024 after the bell in the present day, demonstrating a strong efficiency marked by vital achievements and strategic developments. Listed below are among the particulars from their earnings report and presentation.

Monetary Highlights of Q1 2024:

- Whole Belongings: Elevated to $9.2 billion, up from $8.8 billion within the earlier quarter, pushed primarily by development in securities associated to the structured certificates program.

- Deposits: Rose to $7.5 billion, a slight improve from $7.3 billion on the finish of This autumn 2023, bolstered by high-yield financial savings and certificates of deposit.

- Mortgage Originations: Remained secure at $1.6 billion, demonstrating the corporate’s constant demand regardless of market fluctuations.

- Internet Income: Barely decreased to $180.7 million from $185.6 million within the prior quarter, attributed to a shift in asset combine and elevated deposit funding prices. This exceeded analyst expectations of $173.9 million.

- Internet Earnings: Improved to $12.3 million, up from $10.2 million within the earlier quarter, reflecting environment friendly operational execution and favorable market circumstances. Once more, this considerably exceeded analyst expectations of $3.9 million.

- Capital and Liquidity: Sturdy with a Tier 1 leverage ratio of 12.5% and substantial protection of uninsured deposits, positioning the corporate effectively above regulatory minimums.

Strategic and Operational Developments:

- Digital Market Financial institution: LendingClub’s positioning as a number one digital market financial institution is strengthened by its excessive Internet Promoter Rating of 80 and a median buyer overview score of 4.83 out of 5 stars, indicating sturdy buyer satisfaction and retention.

- Progressive Product Choices: The corporate has successfully expanded its product vary, specializing in offering lower-cost credit score choices to shoppers burdened by high-interest debt. This strategic path shouldn’t be solely aligned with market wants but additionally enhances LendingClub’s aggressive edge.

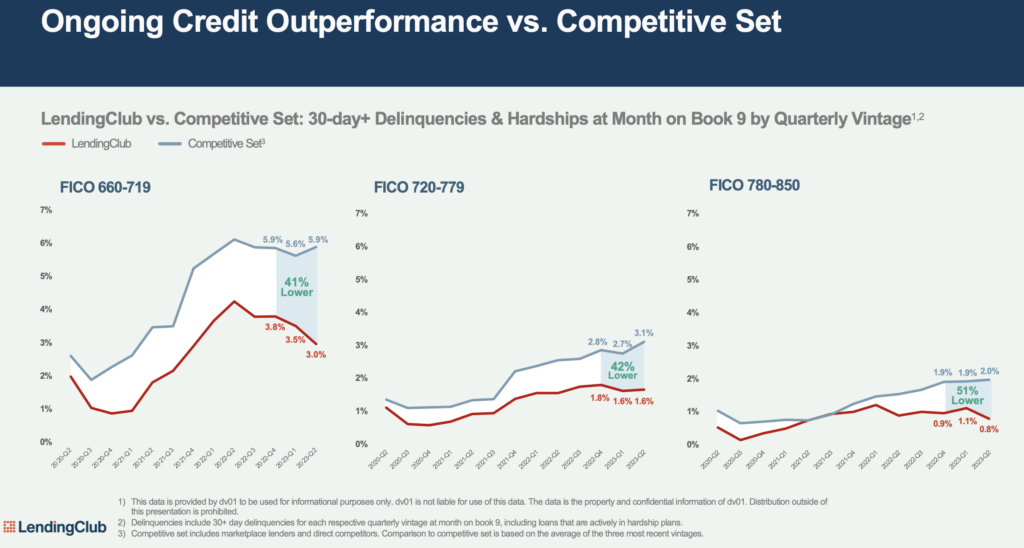

- Threat Administration: Demonstrated decrease delinquency charges in comparison with the aggressive set, with proactive measures in place to handle credit score danger successfully. That is mirrored of their superior efficiency metrics equivalent to decrease web charge-off ratios throughout varied FICO rating segments.

Ahead-Wanting Statements and Steering:

- Q2 2024 Projections: LendingClub expects mortgage originations to vary from $1.6 billion to $1.8 billion and anticipates Pre-Provision Internet Income (PPNR) between $30 million and $40 million. This steering accounts for ongoing strategic initiatives and market circumstances anticipated to affect operational efficiency.

- Lengthy-Time period Technique: The corporate stays dedicated to increasing its suite of economic merchandise and enhancing digital capabilities to higher serve its rising buyer base, reinforcing its market place as a number one innovator within the fintech house.

LendingClub’s Q1 2024 monetary outcomes replicate a strong efficiency underscored by strategic development initiatives and prudent monetary administration. Traders had been happy with the earnings report, the inventory value was up 4% in after-hours buying and selling in the present day.

[ad_2]