[ad_1]

Yesterday (April 24, 2024), the Australian Bureau of Statistics (ABS) launched the most recent – Shopper Worth Index, Australia – for the March-quarter 2024. The info confirmed that the inflation charge continues to fall – down to three.6 per cent from 4 per cent in step with world provide traits. There may be nothing on this quarterly launch that may justify additional rate of interest rises. Regardless of that actuality the nationwide broadcaster has wheeled out a couple of financial institution and/or monetary market economists who declare we can’t rule out additional rate of interest rises. That’s their want as a result of it improves the underside line of their corporations. However it’s arrant nonsense primarily based on the fact and it’s a pity that the nationwide broadcaster can’t current a extra balanced view on this.

The abstract, seasonally-adjusted Shopper Worth Index outcomes for the March-quarter 2024 are as follows:

- The All Teams CPI rose by 1.0 per cent for the quarter (up from 0.6 final quarter).

- The All Teams CPI rose by 3.6 per cent over the 12 months (down from 4 per cent final quarter).

- The Trimmed imply collection rose by 1 per cent for the quarter (up from 0.8) and 4 per cent over the earlier yr (down from 4.2 per cent).

- The Weighted median collection rose by 1.1 per cent (up from 0.9) for the quarter and 4.4 per cent over the earlier yr (regular).

- Meals and non-alcoholic drinks rose by 3.76 per cent (4.46 per cent in December).

- Clothes and footwear regular at 0.42 per cent (-1.11 in December).

- Housing 4.87 per cent (6.12 per cent in December).

- Furnishings and family gear 0.17 per cent (-.025 per cent in December).

- Well being 4.12 per cent (5.13 per cent in December).

- Transport 3.55 per cent (3.65 per cent in December).

- Communications 1.8 per cent (2.2 per cent in December).

- Recreation and tradition 0.2 per cent (0.5 per cent in December).

- Schooling 5.2 per cent (4.7 per cent in December).

- Insurance coverage and monetary companies regular at 8.2 per cent.

The ABS Media Launch (April 24, 2024) – CPI rose 1.0% within the March 2024 quarter – famous that:

Yearly, the CPI rose 3.6 per cent to the March 2024 quarter. Whereas costs continued to rise for many items and companies, annual CPI inflation was down from 4.1 per cent final quarter and has fallen from the height of seven.8 per cent in December 2022. …

Essentially the most important contributors to the March quarter rise have been Schooling (+5.9 per cent), Well being (+2.8 per cent), Housing (+0.7 per cent), and Meals and non-alcoholic drinks (+0.9 per cent) …

Rental costs rose 2.1 per cent for the quarter in step with low emptiness charges throughout the capital cities. Rents proceed to extend at their quickest charge in 15 years …

So a couple of observations:

1. The annual inflation charge continues to fall as the provision constraints throughout most elements ease.

2. Housing inflation has fallen from 10.7 per cent in December 2022 to 4.8 per cent in March 2024, hire inflation continues to rise.

3. Whereas housing contributed 0.23 factors to the general quarterly determine, rents contributed 0.17 factors – so the dominant part.

4. The hire inflation is because of tight provide (a mixture of a ridiculously quick inhabitants progress spawned by a lot bigger immigration numbers over the past yr) and a failure by governments to put money into social housing over the past a number of many years.

5. Nevertheless, given the tight provide, the hire will increase are being pushed by the RBA’s personal charge hikes as landlords in a decent housing market simply move on the upper borrowing prices – so the so-called inflation-fighting charge hikes are actually a big power in driving inflation.

This graph reveals that housing inflation peaked within the December-quarter 2022 and has been steadily declining ever since.

Nevertheless, the rental sub-component has been rising kind of for the reason that RBA began mountaineering charges and is now the key purpose the housing inflation charge remains to be round 4.8 per cent each year.

6. The schooling part is being pushed by the large hikes in non-public education charges and we will conjecture that the mother and father are more likely to be the recipients of the flush of curiosity revenue on their wealth holdings, whereas the RBA punishes the decrease revenue teams who maintain mortgages. A significant fairness catastrophe.

4. Notice that fiscal coverage measures with respect to electrical energy costs subsidies proceed to scale back that stress. The Federal authorities might have executed rather more to alleviate the stress on households of those short-term cost-of-living rises over the past two years.

The overall conclusion is that the worldwide elements that have been accountable for the inflation pressures are abating pretty shortly because the world adapts to Covid, Ukraine and OPEC revenue gouging.

The ABC information report on the information launch – Annual inflation slows to three.6 per cent as larger than anticipated worth rise in March quarter guidelines out early charge reduce hopes (April 24, 2024) – selected to cite an economist from one of many large 4 banks in Australia who claimed that:

You may’t write off the opportunity of the subsequent transfer being a hike relatively than a reduce …

And one other monetary establishment economist mentioned:

This inflation knowledge will definitely renew a few of that debate round whether or not we really must see larger rates of interest …

After all these characters would sow doubt and counsel one other hike wouldn’t be implausible.

They’re hardly ‘unbiased’ or impartial commentators, given their using establishments have benefitted significantly from the current charge hikes.

I do know some readers have been skeptical of my earlier statements that the rising rates of interest have been good for the banks.

Their argument appears to be that the return on fairness has taken a success since 2022 because of the 11 charge hikes since Could 2022 by the RBA.

Nicely the information helps my conclusion pretty definitively.

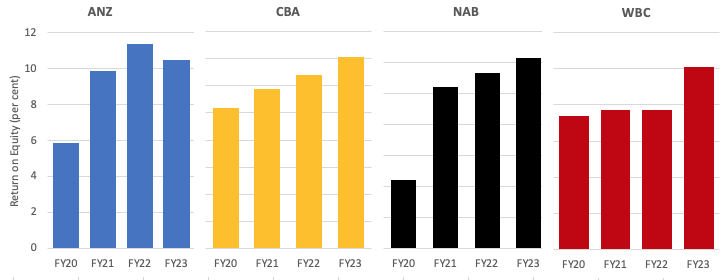

Right here is the information for the final 4 fiscal years for the large 4 banks in Australia who dominate the non-competitive banking sector.

ANZ took a slight dip in charge of return on fairness in FY23 however relative to FY20 and FY21 they’re nonetheless producing large returns.

General, the large 4 banks elevated their return on fairness by 125 foundation factors in 2023 to generate 12 per cent general.

Their internet curiosity margin rose 11 foundation factors to 1.85 per cent.

Their incomes rose 8.2 per cent to $A31.99 billion.

A 12 per cent return on fairness is ridiculously excessive and tells us that the diploma of competitors is low in that sector.

The mania for extra financial coverage tightening is loopy.

The narrative supplied is both that yesterday’s knowledge revealed that the inflation charge was above forecast or that it isn’t falling shortly sufficient.

Take into consideration that for a second.

Which forecast? The financial institution economists who frequently get issues fallacious.

Falling shortly sufficient – the inflation charge has fallen from 7.8 per cent within the December-quarter 2022 to three.6 per cent within the March-quarter 2024.

Between that point it has fallen every quarter by:

March-quarter 2023 – 0.8 factors

June-quarter 2024 – 0.8 factors

September-quarter 2024 – 0.9 factors

December-quarter 2023 – 1.3 factors

March-quarter 2024 – 0.4 factors

The present quarter would have fallen rather more if the rents inflation hadn’t accelerated.

Who’s guilty for that? See above.

Developments in inflation

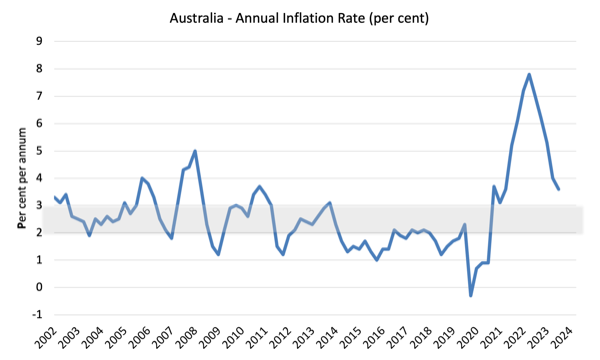

Over the 12 months to December the inflation charge was 3.6 per cent (down from 4).

The height was within the December-quarter 2022 when the inflation charge excessive 7.8 per cent.

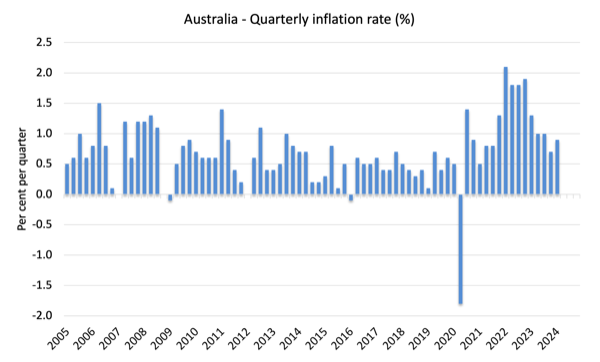

The next graph reveals the quarterly inflation charge for the reason that March-quarter 2005.

The following graph reveals the annual headline inflation charge for the reason that first-quarter 2002. The shaded space is the RBA’s so-called targetting vary (however learn beneath for an interpretation).

What’s driving inflation in Australia?

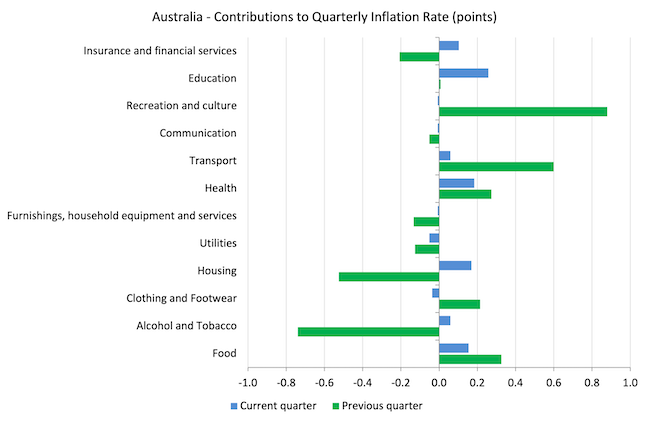

The next bar chart compares the contributions to the quarterly change within the CPI for the March-quarter 2024 (blue bars) in comparison with the December-quarter 2023 (inexperienced bars).

Notice that Utilities is a sub-group of Housing and are considerably impacted by authorities administrative choices, which permit the privatised corporations to push up costs every year, often effectively in extra of CPI actions.

One of many essential drivers – housing – arises from the provision scarcity the place the years of neglect by governments in supplying enough housing for low-income households is now coming residence to roost.

Nevertheless, that contribution fell considerably within the final quarter relative to the September-quarter 2023.

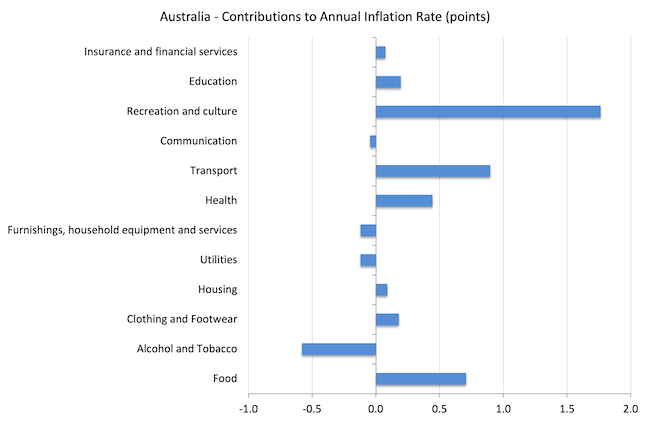

The following graph reveals the contributions in factors to the annual inflation charge by the assorted elements.

The Recreation and tradition elements displays the growth in worldwide journey following the Covid restrictions easing.

It is going to drop out within the coming quarters which is able to drive the annual inflation charge down considerably.

Inflation and Anticipated Inflation

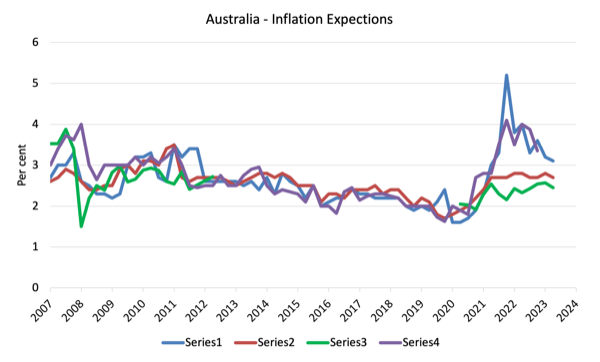

The next graph reveals 4 measures of anticipated inflation produced by the RBA from the March-quarter 2005 to the March-quarter 2023.

The 4 measures are:

1. Market economists’ inflation expectations – 1-year forward.

2. Market economists’ inflation expectations – 2-year forward – so what they suppose inflation might be in 2 years time.

3. Break-even 10-year inflation charge – The common annual inflation charge implied by the distinction between 10-year nominal bond yield and 10-year inflation listed bond yield. It is a measure of the market sentiment to inflation danger. That is thought-about probably the most dependable indicator.

4. Union officers’ inflation expectations – 2-year forward – this collection hasn’t been up to date for the reason that September-quarter 2023.

However the systematic errors within the forecasts, the value expectations (as measured by these collection) are actually falling.

Within the case of the Market economists’ inflation expectations – 2-year forward and the Break-even 10-year inflation charge, the expectations stay effectively inside the RBA’s inflation targetting vary (2-3 per cent) and present no indicators of accelerating.

So all of the speak now’s that inflation shouldn’t be falling quick sufficient – and that declare is accompanied by claims that the longer it stays above the inflation targetting vary, the extra doubtless it’s {that a} wage-price spiral and/or accelerating (unanchored) expectations will drive the speed up for longer.

Neither declare could be remotely justified given the information.

Implications for financial coverage

What does this all imply for financial coverage?

The Shopper Worth Index (CPI) is designed to mirror a broad basket of products and companies (the ‘routine’) that are consultant of the price of dwelling. You may study extra concerning the CPI routine HERE.

The RBA’s formal inflation concentrating on rule goals to maintain annual inflation charge (measured by the buyer worth index) between 2 and three per cent over the medium time period.

Nevertheless, the RBA makes use of a variety of measures to determine whether or not they imagine there are persistent inflation threats.

Please learn my weblog submit – Australian inflation trending down – decrease oil costs and subdued economic system – for an in depth dialogue about the usage of the headline charge of inflation and different analytical inflation measures.

The RBA doesn’t depend on the ‘headline’ inflation charge. As a substitute, they use two measures of underlying inflation which try and internet out probably the most unstable worth actions.

The idea of underlying inflation is an try and separate the pattern (“the persistent part of inflation) from the short-term fluctuations in costs. The primary supply of short-term ‘noise’ comes from “fluctuations in commodity markets and agricultural situations, coverage adjustments, or seasonal or rare worth resetting”.

The RBA makes use of a number of totally different measures of underlying inflation that are usually categorised as ‘exclusion-based measures’ and ‘trimmed-mean measures’.

So, you’ll be able to exclude “a specific set of unstable objects – specifically fruit, greens and automotive gas” to get a greater image of the “persistent inflation pressures within the economic system”. The primary weaknesses with this methodology is that there could be “massive short-term actions in elements of the CPI that aren’t excluded” and unstable elements can nonetheless be trending up (as in power costs) or down.

The choice trimmed-mean measures are in style amongst central bankers.

The authors say:

The trimmed-mean charge of inflation is outlined as the common charge of inflation after “trimming” away a sure share of the distribution of worth adjustments at each ends of that distribution. These measures are calculated by ordering the seasonally adjusted worth adjustments for all CPI elements in any interval from lowest to highest, trimming away those who lie on the two outer edges of the distribution of worth adjustments for that interval, after which calculating a mean inflation charge from the remaining set of worth adjustments.

So that you get some measure of central tendency not by exclusion however by giving decrease weighting to unstable components. Two trimmed measures are utilized by the RBA: (a) “the 15 per cent trimmed imply (which trims away the 15 per cent of things with each the smallest and largest worth adjustments)”; and (b) “the weighted median (which is the value change on the fiftieth percentile by weight of the distribution of worth adjustments)”.

So what has been occurring with these totally different measures?

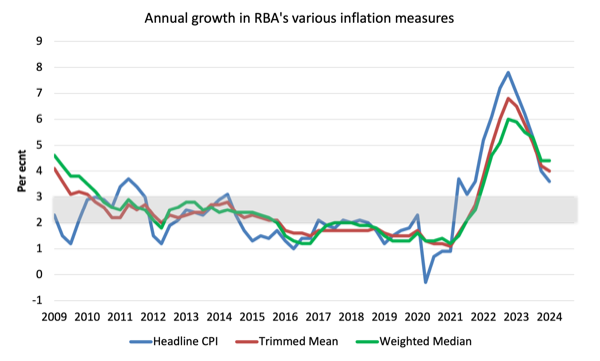

The next graph reveals the three essential inflation collection revealed by the ABS for the reason that March-quarter 2009 – the annual share change within the All objects CPI (blue line); the annual adjustments within the weighted median (inexperienced line) and the trimmed imply (crimson line).

The RBAs inflation targetting band is 2 to three per cent (shaded space). The info is seasonally-adjusted.

The three measures are in annual phrases:

1. The All Teams CPI rose by 1.0 per cent for the quarter (up from 0.6 final quarter) and three.6 per cent over the 12 months (down from 4 per cent final quarter).

2. The Trimmed imply collection rose by 1 per cent for the quarter (up from 0.8) and 4 per cent over the earlier yr (down from 4.2 per cent).

3. The Weighted median collection rose by 1.1 per cent (up from 0.9) for the quarter and 4.4 per cent over the earlier yr (regular).

Tips on how to we assess these outcomes?

1. The RBA’s most well-liked measures stay outdoors the targetting vary and so they have been utilizing that truth to justify their charge hikes since Could 2022 though the elements which have been driving the inflation till late 2022 weren’t delicate to the rate of interest will increase.

2. In addition they claimed the NAIRU was 4.25 per cent and with unemployment secure at round 3.9 per cent, they thought-about that justified additional charge rises. Nevertheless, if inflation is falling persistently with a secure unemployment charge then the NAIRU should be beneath the present charge of three.9 per cent.

3. There is no such thing as a proof that inflationary expectations are accelerating – fairly the other and that has been the case for some months now.

4. There is no such thing as a important wages stress.

5. A significant contributor to the present scenario – rents – are, partly, being pushed up by the rate of interest rises.

7. There is no such thing as a justification for any additional charge rises, particularly given the slowdown in retail gross sales famous above.

Conclusion

The newest CPI knowledge confirmed that inflation continues to say no in Australia in step with traits across the globe.

This was all the time a transitory, supply-side inflation, which meant that demand-side measures (rate of interest hikes) have been completely inappropriate.

That’s sufficient for at this time!

(c) Copyright 2024 William Mitchell. All Rights Reserved

[ad_2]